Blog

Avoid HMRC Penalties in 2026: Recordkeeping Checklist for SMEs

Magnolia Roy | 24 April 2026

Many UK SMEs assume HMRC penalties only happen when deadlines are missed. In reality, poor recordkeeping is one of the main reasons businesses face compliance checks, disputed returns, and avoidable costs. This practical guide explains what records to keep, how long to keep them, common mistakes to avoid, and how to stay HMRC-ready in 2026.

Many UK businesses assume HMRC penalties only happen when deadlines are missed. In reality, poor recordkeeping is one of the most common reasons businesses face compliance checks, unexpected tax bills, and avoidable HMRC penalties.

If your records are incomplete, inconsistent, unreadable, or difficult to produce, HMRC may question your returns, estimate the tax due, and charge penalties where appropriate .

For UK SMEs, the safest way to reduce the risk of penalties in 2026 is simple:keep accurate records, retain them for the required period, and make sure your system is organised enough to produce evidence when needed.

TL;DR

Most HMRC penalties linked to recordkeeping are preventable.

The real problem is often incomplete records, missing evidence, or poor systems.

To avoid HMRC penalties, UK SMEs should:

- keep complete income and expense records

- maintain VAT and payroll evidence

- retain records for the correct period

- move to digital systems where required

- review records regularly before filing

In 2026, this matters even more as digital recordkeeping requirements continue to expand.

Why Recordkeeping Matters for UK SMEs

Most businesses do not face HMRC penalties because they intentionally underpay tax.

Problems usually start because records are disorganised.

- Receipts are stored in emails.

- Sales data sits in one system.

- Payroll sits in another.

- VAT records are incomplete.

Then a return is submitted using figures that cannot be fully supported.

That is when penalties become a real risk.

HMRC expects businesses to keep records that are:

- accurate

- complete

- readable

- easy to produce during a compliance check

If records are missing or unclear, HMRC may challenge the return and charge penalties even if the mistake was not deliberate .

What Records Does HMRC Expect You to Keep?

The records you must keep depend on your business structure.

If you are a sole trader or partnership, HMRC expects records of:

- all sales and income

- all business expenses

- VAT records if registered

- PAYE records if you employ staff

- personal income records for Self Assessment

If you run a limited company, you must keep accounting records showing:

- all money received

- all money spent

- bank statements

- invoices

- supporting correspondence

- documents needed for annual accounts and Company Tax Returns

Without these records, it becomes much harder to defend the accuracy of your tax returns and avoid HMRC penalties.

The Real Problem Behind HMRC Penalties

Many businesses focus only on late filing penalties, but poor records create much bigger risks.

Weak recordkeeping can lead to:

- incorrect returns

- unsupported expense claims

- VAT mistakes

- payroll errors

- extra tax assessments

- longer HMRC compliance checks

In some cases, HMRC can charge up to £3,000 for each failure to keep or preserve adequate records in relation to a return or claim.

Employers operating PAYE may also face penalties of up to £3,000 if payroll records are not properly maintained.

On top of that, if an error happens because reasonable care was not taken, HMRC says penalties may be:

- 0% to 30% of extra tax due for careless errors

- 20% to 70% for deliberate errors

- 30% to 100% for deliberate and concealed errors

That is why avoiding HMRC penalties starts with good recordkeeping long before filing deadlines.

Recordkeeping Checklist to Avoid HMRC Penalties in 2026

1. Keep Full Records of Sales and Income

Your records should clearly show where income came from and when it was earned or received.

This may include:

- invoices issued

- till rolls or EPOS reports

- contracts

- payment confirmations

- bank receipts

- credit notes

Keeping complete income records is essential because HMRC expects businesses to support the income figures reported on returns. Missing records can trigger questions and increase the risk of HMRC penalties.

2. Keep Evidence for Every Business Expense

Every expense claimed should be backed by evidence.

This may include:

- supplier invoices

- receipts

- mileage logs

- bank statements

- card statements

- payment confirmations

- contracts for recurring services

If expense evidence is missing, HMRC may disallow the cost or question the return. Unsupported expense claims are a common cause of compliance problems and potential penalties.

3. Maintain Proper VAT Records

VAT registered businesses must keep proper VAT records and, unless exempt, maintain certain records digitally under Making Tax Digital for VAT.

VAT records may include:

- VAT account or electronic account

- VAT invoices issued and received

- import and export VAT documents

- VAT adjustments

- reverse charge evidence

Late VAT submissions can trigger penalty points. Once the threshold is reached, HMRC may issue a £200 penalty, followed by further penalties for repeated failures.

Poor VAT records significantly increase the risk of HMRC penalties.

4. Keep PAYE and Payroll Records

If you employ staff, payroll records must show that wages and deductions were reported correctly.

These records may include:

- employee pay records

- deductions

- statutory payments

- benefits and expenses records

- pension contributions

- HMRC correspondence

HMRC says payroll records must be kept for 3 years from the end of the tax year they relate to.

Incomplete payroll records can result in reporting issues and HMRC penalties.

5. Separate Business and Personal Transactions

One of the simplest ways to improve recordkeeping is to separate business and personal spending.

Use:

- A dedicated business bank account

- Clear labels for mixed-use expenses

- Documentation for the business portion of shared costs

Mixing business and personal transactions creates weak audit trails and makes it harder to support the figures in your return, increasing the likelihood of HMRC penalties.

6. Keep Records Searchable and Backed Up

It is not enough to store records somewhere.

You must be able to produce them when needed.

A reliable recordkeeping system should make it easy to:

- search by supplier, customer, or date

- match receipts to transactions

- export reports

- store copies securely

- back up digital data

HMRC expects records to be accurate, complete, and readable. If you cannot quickly produce evidence, that can still lead to HMRC penalties.

7. Know How Long to Keep Records

Keeping records for the right amount of time is essential.

Here are the usual retention periods:

Business Area | Minimum Retention Period |

Self-employed records | At least 5 years after the 31 January submission deadline |

Limited company records | 6 years from the end of the financial year |

PAYE payroll records | 3 years from the end of the tax year |

Expenses and benefits records | 3 years from the end of the tax year |

VAT records | Usually 6 years |

Deleting records too early can cause problems if HMRC asks for evidence later, increasing exposure to HMRC penalties.

These are the usual minimum retention periods, but businesses may need to keep records longer in some circumstances, such as where returns are filed late or HMRC is checking earlier periods.

Digital Recordkeeping and Making Tax Digital in 2026

In 2026, digital recordkeeping matters even more.

For VAT, digital records and software filing are already standard for VAT registered businesses unless exempt.

For Income Tax, Making Tax Digital is now in effect from 6 April 2026 for sole traders and landlords whose qualifying income from self-employment and property exceeds £50,000, based on turnover before expenses from the previous Self Assessment return.

HMRC confirms that those brought into MTD from 6 April 2026 will not receive penalty points for late quarterly updates during the first tax year (2026–27). However, penalties may still apply for late tax returns and late payment.

This means:

- keeping digital records

- using compatible software

- submitting updates digitally

If your records are still spread across paper receipts, bank downloads, and manual spreadsheets with no consistent process, 2026 is the year to fix that before HMRC penalties become the expensive prompt.

Common Recordkeeping Mistakes That Lead to HMRC Penalties

Some of the most common mistakes include:

Missing receipts

Bank transactions alone may not be enough to prove the expense.Filing figures that do not match records

Manual adjustments and unreconciled data can create inaccuracies.Mixing personal and business costs

This weakens your evidence trail.Not keeping records long enough

Deleting records too soon can create issues during compliance checks.Leaving bookkeeping until year end

Missing evidence is much harder to recover later.

Each of these issues increases the risk of HMRC penalties, extra HMRC queries, and unnecessary stress.

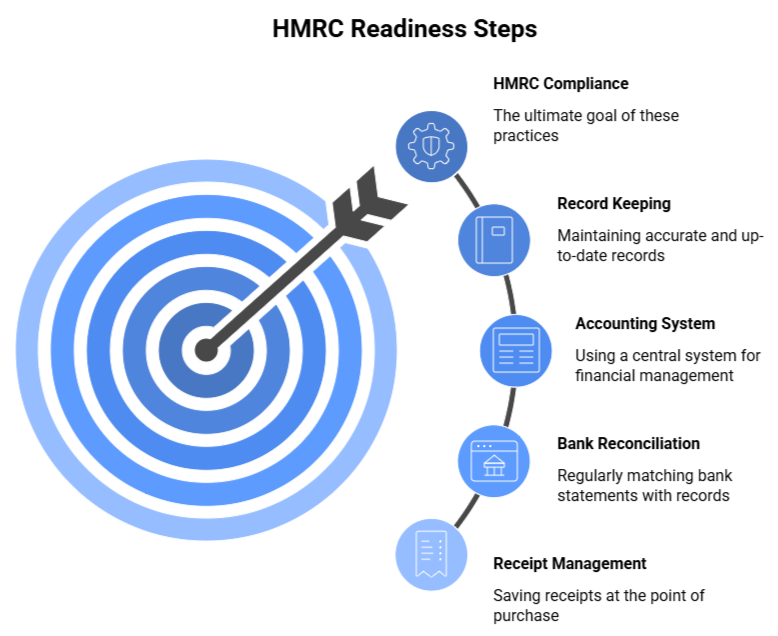

Practical Steps to Stay HMRC-Ready

When to Get Help

You do not need to wait until HMRC contacts you.

If any of these apply, it may be time to review your systems:

- your bookkeeping is behind

- you are unsure what records HMRC expects

- VAT records do not match returns

- payroll records are spread across multiple files

- you are moving to digital recordkeeping

- you cannot quickly produce records when needed

Good recordkeeping is not just about admin.

It helps reduce compliance risk, improve accuracy, and protect your business from HMRC penalties.

If you are unsure whether your records are HMRC-ready, AMS Admin Services can help you review your processes, organise your bookkeeping, and improve compliance before small issues turn into costly HMRC penalties.

FAQs

1. What records should a small business keep to avoid HMRC penalties?

A small business should keep records of sales, expenses, VAT, payroll, invoices, receipts, bank statements, and supporting correspondence to reduce the risk of HMRC penalties.

2. How long should SMEs keep records?

Self-employed records generally need to be kept for at least 5 years, limited company records for 6 years, and payroll records for 3 years.

3. Does Making Tax Digital affect recordkeeping?

Yes. VAT registered businesses must keep certain records digitally, and from April 2026 some sole traders and landlords must also maintain digital records under MTD rules.