Blog

Corporation Tax UK in 2026: Rates, Reliefs and Deadlines Explained

Magnolia Roy | 10 April 2026

Corporation tax UK is a key obligation for small businesses. This 2026 guide explains current tax rates, deadlines, how corporation tax is calculated, and practical ways to manage your tax liability while staying compliant with HMRC rules.

What is corporation tax and who needs to pay it?

Corporation Tax is the tax UK limited companies pay on their taxable profits. This can include trading profits, investment income, and chargeable gains.

If you run a limited company in the UK, you usually need to calculate your Corporation Tax, report it to HMRC, and pay what is due.

For business owners, this is not optional. It is a legal responsibility linked to your company’s accounting period.

Corporation Tax rates in the UK for 2026

For the 2026 tax year, corporation tax in the UK follows a tiered system based on profit levels.

Corporation tax bands

Profit Level | Corporation Tax Rate |

Up to £50,000 | 19% (small profits rate) |

£50,001 to £250,000 | Marginal relief applies |

Over £250,000 | 25% (main rate) |

- Companies earning £50,000 or less pay corporation tax at 19%

- Companies above £250,000 pay the full 25% rate

- Profits between these thresholds are adjusted using marginal relief to avoid a sharp jump in tax

This structure is designed to support small businesses while scaling tax gradually as profits grow.

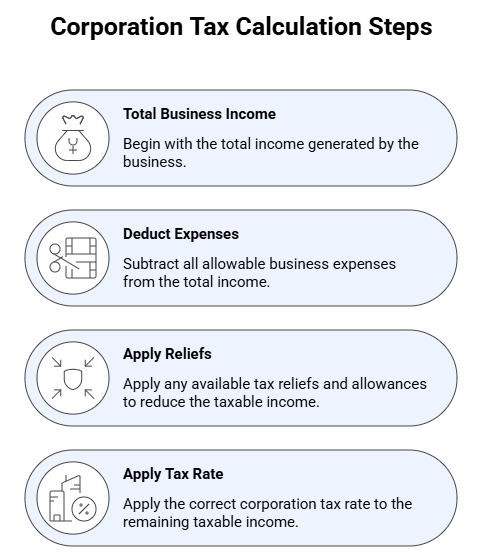

How corporation tax is calculated

Corporation tax is calculated on taxable profits, not total revenue.

What counts as taxable profits?

- Trading profits from your business

- Investment income

- Profits from selling assets

In simple terms, the process works like this:

Income minus allowable business costs = taxable profit

Taxable profit × applicable Corporation Tax rate = Corporation Tax liability

This final figure is the amount your company must pay to HMRC.

Basic corporation tax calculation

This final figure is your corporation tax liability.

When do you pay corporation tax?

Corporation tax follows strict deadlines.

Key deadlines

Task | Deadline |

Register for corporation tax | Within 3 months of starting business activity |

Pay corporation tax | 9 months and 1 day after the end of your accounting period |

File CT600 return | Within 12 months of the end of your accounting period |

Missing these deadlines can lead to HMRC penalties, interest charges, and avoidable compliance issues.

Why corporation tax matters for small businesses

Corporation Tax affects more than just your tax bill.

It can directly impact your:

- Cash flow

- Profit retention

- Growth decisions

- Director withdrawals

When does Corporation Tax start creating pressure?

This usually shows up when:

- Your profits increase but cash is tied up in unpaid invoices

- You do not set money aside for tax during the year

- You take too much cash out of the business before accounting for tax

This creates pressure when the payment deadline arrives.

Many small businesses aren’t unprofitable, they struggle because tax bills arrive unplanned

Common corporation tax mistakes

1. Not setting aside cash for tax

Many businesses treat profit as available cash. That often leads to a shock when the Corporation Tax bill becomes due.

2. Incorrect expense claims

Not every business cost is allowable for Corporation Tax. Incorrect claims can lead to errors, amendments, or HMRC questions later.

3. Ignoring marginal relief

Businesses between £50,000 and £250,000 often miscalculate corporation tax due to marginal relief complexity.

4. Late filing

Late CT600 submissions can lead to penalties and increase the risk of further HMRC attention.

Corporation tax reliefs and allowances

Corporation Tax is not only about what you owe. It is also about making sure you claim the reliefs and allowances your company is entitled to use.

Common reliefs

Relief Type | What It Does |

Capital allowances | Deduct cost of equipment and assets |

R&D tax relief | May reduce tax for eligible research and development activity |

Loss relief | Offset losses against profits |

Annual Investment Allowance | Deduct qualifying investments |

Using these correctly can significantly reduce your corporation tax bill.

Example in practice:

A growing business that invests in qualifying equipment, incurs eligible development costs, or carries forward losses may be able to reduce its tax bill through the correct use of available reliefs.

Corporation tax and business growth

Corporation tax becomes more important as your business grows.

Why it matters more over time

- Higher profits move you into the 25% tax band

- Marginal relief calculations become more complex

- Cash flow planning becomes critical

- Extraction decisions need more planning

For growing UK businesses, Corporation Tax is not just a compliance issue. It becomes part of how you plan growth, manage cash, and make better financial decisions.

How to manage corporation tax properly

Practical approach:

- Track profits monthly, not annually

- Set aside tax reserves regularly

- Review expenses for eligibility

- Plan ahead before profit increases

- Align dividend decisions with tax liabilities

This helps keep your Corporation Tax manageable, predictable, and less likely to disrupt cash flow.

Bring Clarity to Your Corporation Tax

At AMS Admin Services, we help UK business owners understand their Corporation Tax position clearly.

That includes helping you:

- Plan your salary and dividends in advance

- Stay fully compliant with HMRC requirements

- Make informed, tax-efficient decisions as your profits grow

Book a clarity call with AMS today and understand exactly how the right financial structure can reduce your corporation tax, improve cash flow, and remove compliance stress.

TL;DR

- Corporation tax is a mandatory tax on company profits in the UK

- Rates for 2026:

- 19% up to £50,000

- Gradual increase between £50,000 and £250,000

- 25% above £250,000

- Payment is due 9 months and 1 day after the end of your accounting period

- Poor planning leads to cash flow issues, not just tax problems

- Reliefs and proper structuring can reduce your corporation tax liability

FAQs

1. What is the corporation tax rate in the UK for 2026?

The corporation tax rate is 19% for profits up to £50,000 and 25% for profits above £250,000. Profits in between are adjusted using marginal relief.

2. When do I need to pay corporation tax?

You must pay corporation tax 9 months and 1 day after the end of your accounting period. Your tax return is due within 12 months.

3. Can I reduce my corporation tax legally?

Yes. You can reduce corporation tax through allowable expenses, capital allowances, R&D relief, and loss relief. These must be applied correctly under HMRC rules.