Blog

Employment Allowance 2026/27: How UK Small Businesses Can Reduce Employer National Insurance

Magnolia Roy | 05 June 2026

Don’t let employer National Insurance eat into your cash flow. Employment Allowance 2026/27 could reduce your employer NIC bill by up to £10,500. This guide explains who can claim, the rules to watch, and how UK SMEs can use the allowance before payroll costs start to bite.

TL;DR

Employment Allowance is one of the main ways eligible UK small businesses can reduce employer Class 1 National Insurance costs in the 2026/27 tax year. Eligible employers can reduce their annual employers’ Class 1 National Insurance liability by up to £10,500 each tax year. HMRC says the allowance is used each time payroll is run, until the £10,500 allowance is used or the tax year ends, whichever comes first.

For 2026/27 payroll planning, the key numbers are: the employer NIC rate above the Secondary Threshold is 15%, and the Secondary Threshold is £96 per week, £417 per month, or £5,000 per year.

For a UK SME founder, the practical goal is simple:

Priority | What to do | Why it matters |

Check eligibility | Confirm whether your business can claim | Not every employer qualifies |

Claim early | Submit the claim through payroll | Earlier claims improve cash flow |

Forecast employer NIC | Budget before hiring or increasing salaries | Payroll costs can rise faster than expected |

What is employer National Insurance?

Employer National Insurance is a payroll cost your business pays to HMRC on top of employee wages.

It is different from employee National Insurance.

You usually pay employer NIC when an employee earns above the relevant employer National Insurance threshold. HMRC calls this the Secondary Threshold. For 2025/26 and 2026/27, the Secondary Threshold is £96 per week, £417 per month, or £5,000 per year.

Simple explanation

Employer NIC is a payroll cost paid by the employer. It is not deducted from the employee’s wages.

Why this matters for UK SMEs

An employee’s salary does not only cost the amount written in the employment contract.

Employee salary | Approximate employer NIC calculation | Approximate employer NIC before allowance |

£20,000 | (£20,000 minus approx. £5,000) x 15% | £2,250 |

£30,000 | (£30,000 minus approx. £5,000) x 15% | £3,750 |

£40,000 | (£40,000 minus approx. £5,000) x 15% | £5,250 |

These are simple annual estimates for planning only. Actual payroll calculations should follow HMRC thresholds, payroll frequency, employee category letter, and director rules where relevant. The 15% employer NIC rate applies above the Secondary Threshold for 2025/26 and 2026/27.

What is Employment Allowance?

Employment Allowance is a relief that allows eligible employers to reduce their annual employer Class 1 National Insurance bill.

HMRC states that eligible employers can reduce their annual employer Class 1 National Insurance liability by up to £10,500. The relief is applied through payroll against employer Class 1 National Insurance.

What does Employment Allowance reduce?

Cost type | Can the allowance reduce it? | Notes |

Employers’ Class 1 National Insurance | Yes | This is the main use |

Employee National Insurance | No | Employee NI is separate |

Corporation Tax | No | It is not a Corporation Tax relief |

VAT | No | It is not a VAT relief |

PAYE income tax deductions | No | PAYE tax is still due |

How much is Employment Allowance in 2025/26 and 2026/27?

Employment Allowance is £10,500 for 2025/26 and 2026/27. HMRC’s employer rates and thresholds guidance lists the allowance as £10,500 for both tax years.

For many small employers, this can remove a large part of the employer NIC bill.

For some smaller payrolls, it may reduce the annual employer NIC bill to zero.

How does Employment Allowance reduce employer NIC?

Employment Allowance reduces employer NIC by offsetting the allowance against employer Class 1 National Insurance each time payroll is run.

HMRC says the allowance is used until the full £10,500 has been used or the tax year ends, whichever happens first.

Example

If the company is eligible, the Employment Allowance can offset the full £8,000 employer NIC bill. This means the employer NIC left to pay for the year would be £0, assuming the employer remains eligible and the liability is qualifying employer Class 1 NIC.

If the employer Class 1 National Insurance bill is lower than the full allowance, the unused amount does not automatically become a cash refund. HMRC guidance says unused Employment Allowance may be used against other PAYE liabilities, and if none are outstanding, an employer may be able to ask HMRC for a repayment.

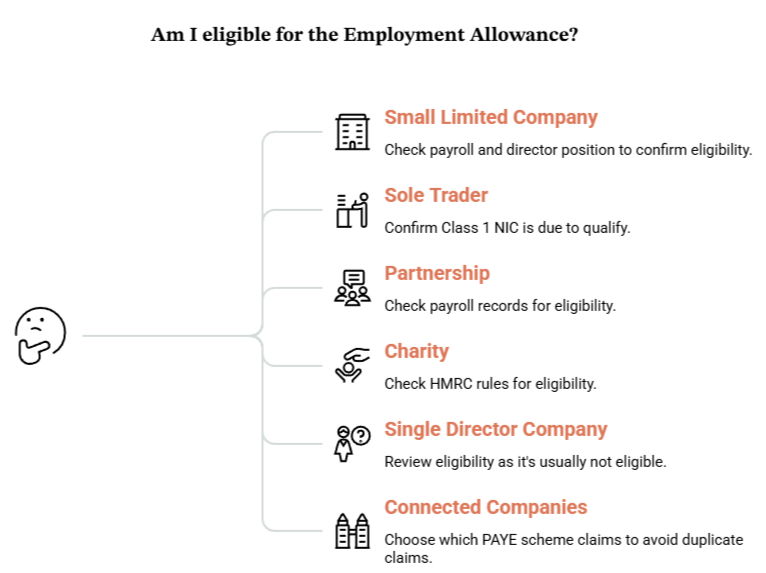

Who can claim Employment Allowance?

Employment Allowance eligibility depends on your business structure, payroll setup, and the type of work your organisation carries out.

HMRC says you can claim Employment Allowance if you are a business or public body and your organisation does less than half of its work in the public sector.

For companies with only one director, HMRC says the company cannot claim if that director is the only employee liable for secondary Class 1 National Insurance.

HMRC also states that charities, including community amateur sports clubs, can claim, and employers of care or support workers may also qualify.

Employment Allowance Eligibility Checklist for Employers

HMRC confirms that self-employed employers can claim if they have employees and pay employer Class 1 NICs on employee earnings. HMRC also confirms that partnerships can claim if they employ anyone and pay employer Class 1 NICs as a result.

What changed from April 2025?

From April 2025, the previous £100,000 employer Class 1 National Insurance limit was removed. This means employers with more than £100,000 in employer Class 1 National Insurance liabilities may be able to claim Employment Allowance if they meet the other eligibility rules.

HMRC says different rules apply if you are claiming Employment Allowance for previous tax years.

This matters because some employers who could not claim under the old £100,000 limit may now need to review their eligibility again.

SME takeaway

Do not assume last year’s answer still applies.

If your payroll has grown, or if you were previously unable to claim because of the old £100,000 employer NIC limit, review your position again for 2025/26 and 2026/27 planning.

How do connected companies affect the claim?

Connected companies need extra care because only one company in a connected group can claim Employment Allowance for the tax year.

HMRC says if two or more companies are connected at the start of the tax year, only one of those companies can qualify for the allowance for that tax year. The companies decide which one claims.

Companies may be connected where:

- One company controls another.

- Companies are under the control of the same person or people.

- Group companies share control arrangements.

HMRC says connected company rules do not apply to sole traders, partnerships, or single companies.

When should you claim?

You need to claim Employment Allowance each tax year.

HMRC says you need to claim every tax year, and you can claim at any time in the tax year. The earlier you claim, the sooner you receive the allowance through reduced employer National Insurance payments.

How to claim Employment Allowance through payroll software

- Check your business is eligible before claiming.

- Confirm no connected company has already claimed for the same tax year.

- Claim through your payroll software.

- The claim is usually submitted to HMRC through an Employer Payment Summary.

- Make sure the allowance is applied only against qualifying employer Class 1 National Insurance.

- Ask your accountant or payroll provider to confirm the claim appears correctly in your PAYE account.

- Keep a record of your eligibility checks in case HMRC asks for evidence.

How can UK SMEs manage employer National Insurance costs in 2026/27?

There are several compliant ways to manage employer National Insurance.

The aim is not to avoid payroll costs artificially. The aim is to plan properly.

1. Use the allowance if eligible

Employment allowance should be checked before you accept employer NIC as a fixed cost.

Many small employers miss savings because they do not review payroll reliefs each year.

2. Forecast before hiring

Before hiring, calculate:

- Gross salary

- Employer NIC

- Pension contributions

- Payroll admin costs

- Holiday pay

- Any bonus or commission structure

A £30,000 salary is not only a £30,000 cost to the company.

3. Review salary levels for directors

Director salaries need careful planning.

For owner-managed companies, salary decisions can affect:

- Employer NIC

- Employee NIC

- Corporation Tax relief

- Dividend planning

- Pension contributions

Do not copy a salary strategy from another founder. Their company structure, profit level, and payroll position may be different.

4. Consider pension contributions

Employer pension contributions may form part of a wider tax-efficient remuneration plan.

This needs advice because pension planning depends on affordability, annual allowance rules, company profits, and the director’s personal position.

5. Keep payroll clean and consistent

Small payroll errors can create bigger problems later.

A simple monthly payroll review should check:

- Employee category letters

- Starters and leavers

- Director status

- Pension deductions

- Employer NIC

- Allowance claimed

- PAYE balance due to HMRC

What should founders watch out for?

The biggest mistake is treating employer NIC as a once-a-year issue.

It affects cash flow every payroll month.

Common problems

Problem | Why it causes stress | Better approach |

Claiming without checking eligibility | HMRC may challenge the claim | Review before submitting |

Forgetting connected companies | More than one company may claim incorrectly | Decide which company claims |

Assuming the allowance gives cash back | It only reduces qualifying liability | Forecast the actual NIC bill |

Ignoring payroll growth | Costs rise as salaries and headcount rise | Build employer NIC into budgets |

Leaving the claim too late | Cash flow benefit is delayed | Claim early in the tax year |

UK SME employer NIC checklist

Use this checklist before your next payroll review or before claiming Employment Allowance:

- Confirm your estimated employer NIC bill for the current tax year.

- Check that the correct Secondary Threshold has been used for 2025/26 or 2026/27.

- Review whether the 15% employer NIC rate has been applied correctly above the Secondary Threshold.

- Confirm whether your company is connected to another company at the start of the tax year.

- Check whether your business meets HMRC’s Employment Allowance eligibility rules.

- Confirm whether the Employment Allowance claim has been submitted for the current tax year.

- Forecast payroll costs for the next 6 to 12 months.

- Ask your accountant to review director salary, dividends, pension contributions, and employer NIC together.

Take Control of Employer NIC Before Payroll Pressure Builds

Employer National Insurance should not feel like a surprise cost at the end of the month.

With the right payroll review, Employment Allowance can help eligible businesses reduce employer Class 1 NIC and plan payroll with more confidence.

At AMS, we help UK small business owners check eligibility, review employer NIC costs, and understand the real cost of payroll before decisions are made.

Planning payroll for 2025/26 or 2026/27?

Speak with AMS before your next payroll run. We’ll review your Employment Allowance position, check your employer NIC exposure, and help you plan payroll costs with confidence.

Frequently Asked Questions

Can a single director company claim?

A company with only one director cannot usually claim if that director is the only employee liable for secondary Class 1 National Insurance. HMRC says a company with only one director must not have that director as the only employee liable for secondary Class 1 National Insurance.

Do I need to claim every year?

Yes. HMRC says employers need to claim every tax year. Claiming earlier helps the allowance reduce employer National Insurance sooner through payroll.

Can connected companies each claim separately?

No. If companies are connected at the start of the tax year, HMRC says only one company can qualify for that tax year. The connected companies decide which company claims.