Blog

Salary vs Dividends UK: A Practical Guide for Company Directors

Magnolia Roy | 03 April 2026

Discover how UK company directors can structure salary vs dividends UK to reduce tax and stay compliant. This practical guide explains HMRC thresholds, common mistakes, and how to balance salary and dividends for long-term financial stability.

What is the most tax-efficient way to pay yourself as a UK company director?

For most UK company directors, the most tax-efficient approach is a combination of a small salary and dividends.

This structure helps you:

- Reduce Income Tax and National Insurance

- Stay compliant with HMRC

- Maintain eligibility for state benefits

Relying only on salary usually increases tax, while relying solely on dividends can create compliance and long-term planning issues.

The real advantage comes from balancing both properly.

The Hidden Importance of Balancing Salary and Dividends

Most founders treat this as a simple choice. It is not.

This decision directly impacts:

- Your personal tax bill

- Your company’s Corporation Tax

- Your entitlement to state benefits

- Your long-term financial planning

In practice, this shows up later, not immediately.

That is where understanding salary vs dividends UK becomes a strategic decision, not just a tax one.

Understanding how directors get paid in the UK

Salary (via PAYE):

A salary is paid through PAYE and:

- Is subject to Income Tax and National Insurance

- Counts as a business expense (reduces Corporation Tax)

- Helps you qualify for state pension

Dividends:

Dividends are paid from profits after Corporation Tax:

- Not subject to National Insurance

- Taxed at dividend tax rates

- Only payable if the company has retained profits

Salary vs Dividends UK: Key differences at a glance

Feature | Salary | Dividends |

Tax type | Income Tax + National Insurance | Dividend Tax only |

Corporation Tax impact | Reduces profits | Paid after tax |

Cash flow timing | Regular monthly | Flexible |

HMRC requirement | PAYE reporting | Dividend vouchers required |

Eligibility | Always allowed | Only from profits |

How to Optimise Your Pay Mix as a UK Company Director?

Most UK directors use this structure:

- Take a small salary up to the National Insurance threshold

- Top up income with dividends

This works because:

- You utilise your Personal Allowance

- You reduce National Insurance

- You benefit from lower dividend tax rates

Putting this into perspective:

Consider a director with £60,000 in company profits. Using the low salary plus dividends approach, their total tax can be substantially lower than taking the same amount purely as salary. Real-world cases consistently show that this method improves take-home pay while staying compliant with HMRC rules.

What the actual HMRC thresholds say (2026/27)

To correctly understand salary vs dividends UK, you need to base decisions on real thresholds.

Key UK tax thresholds:

- Personal Allowance: £12,570

- Basic Rate Band (20%): up to £50,270 taxable income.

- Dividend Allowance: £500

These thresholds are fixed through at least April 2028 due to UK tax policy.

What This Means For Salary vs Dividend UK Planning

In most cases, directors combine salary and dividends to stay tax-efficient.

A common approach is:

- Pay a salary within the range of the National Insurance threshold and the Personal Allowance

- Take additional income as dividends from company profits

This helps you:

- Utilise your Personal Allowance

- Reduce exposure to National Insurance

- Benefit from lower dividend tax rates

It is also important to note:

Dividends are paid from profits after Corporation Tax, so your company must first be profitable before any dividends can be issued.

Dividend Tax Rates UK (2026/27)

Dividend tax is applied after your Personal Allowance and £500 dividend allowance are used.

Tax Band | Dividend Tax Rate |

Basic Rate | 10.75% |

Higher Rate | 35.75% |

Additional Rate | 39.35% |

Your dividend tax band depends on your total income, including salary and dividends combined.

Adjusting Salary and Dividends Based on Your Situation

This is not a one-size-fits-all decision.

Your optimal mix changes based on:

1. Profit levels

No profits means no dividends. This is non-negotiable.

2. Other income sources

Rental income or side income can push you into higher tax bands.

3. Pension planning

Higher salaries can increase pension contributions and benefits.

4. Mortgage applications

Lenders sometimes prefer salary stability over dividends.

5. Future exit plans

Your remuneration strategy can impact how you structure long-term tax planning.

What are the risks of getting salary vs dividend UK wrong?

Most issues do not show up immediately. They surface later.

Common mistakes:

- Taking dividends without sufficient profits

- Ignoring PAYE obligations

- Not documenting dividend payments properly

- Over-relying on dividends and missing state benefits

According to HMRC compliance guidance, incorrect dividend handling can trigger penalties and enquiries.

This is not just about tax. It is about staying compliant without stress.

Why dividends are not always better

There is a common belief that dividends are tax-efficient, but incomplete on their own.

Dividends do not: | Salary does: |

Count as earned income for some benefits | Help you qualify for state pension |

Build National Insurance credits | Strengthen financial credibility |

Provide employment protections | Support long-term planning |

The best strategy is not choosing one. It is balancing both.

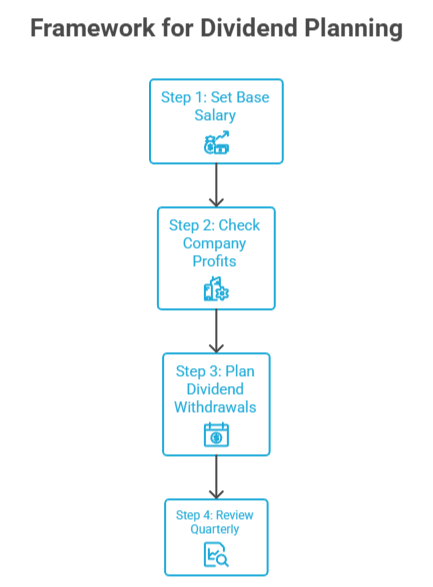

Step-by-Step Guide to Finding Your Optimal Salary vs Dividend Mix

Instead of guessing, use this framework:

Tax efficiency is not static. It evolves with your business.

The real insight most founders miss

Salary vs dividends UK is not about minimising tax today. It is about building a sustainable financial structure.

Short-term savings can create long-term problems if you ignore:

- Compliance

- Cash flow timing

- Personal financial goals

Take Control of Your Director Pay

At AMS Admin Services, we help UK business owners turn uncertainty into clarity.

Instead of scrambling at year-end, you can:

- Plan your salary and dividends ahead of time

- Stay fully compliant with HMRC

- Make confident, tax-efficient decisions

Book a clarity call with AMS today and see exactly how the right salary vs dividend mix can save you tax and reduce compliance stress.

TL;DR Summary

- The best approach to salary vs dividends UK is a combination of both

- Salary reduces Corporation Tax but triggers National Insurance

- Dividends are tax-efficient but require profits

- Most directors use a low salary plus dividends strategy

- Your ideal mix depends on profits, goals, and personal circumstances

- Regular review is essential to stay tax-efficient and compliant

FAQs

1. Is salary or dividends better in the UK?

Neither is better on its own. The most tax-efficient strategy in the salary vs dividends UK decision is usually a combination of both, structured around your income and company profits.

2. Can I take dividends without paying a salary?

Yes, but it is not always advisable. You may miss out on National Insurance credits and certain benefits. A small salary is often still recommended in the salary vs dividends UK approach.

3. How often should I review my salary vs dividends UK strategy?

At least quarterly. Changes in profits, tax rules, or personal income can affect your optimal structure. Regular reviews help you stay efficient and compliant.