Blog

UK VAT Schemes for Small Businesses: 2026 Guide

Magnolia Roy | 22 May 2026

Choosing the right VAT scheme can make a real difference to cash flow, admin, and compliance for UK small businesses. This guide explains the main UK VAT schemes, including Flat Rate, Cash Accounting, Annual Accounting, Margin Scheme, and the VAT Capital Goods Scheme, so you can understand which option may suit your business.

TL;DR:

UK VAT schemes are HMRC-approved ways for VAT-registered businesses to calculate, report, or pay VAT.

The right scheme depends on how your business works, including your cash flow, customer payment timing, taxable turnover, costs, and the type of goods or services you sell.

For most UK SMEs, the main VAT schemes to review are the VAT Flat Rate Scheme, VAT Cash Accounting Scheme, VAT Annual Accounting Scheme, and VAT Margin Scheme. Businesses buying high-value assets should also be aware of the VAT Capital Goods Scheme.

A simple way to think about it:

- If customers pay late, review the VAT Cash Accounting Scheme.

- If reducing admin is the main priority, review the VAT Flat Rate Scheme or VAT Annual Accounting Scheme.

- If you sell eligible second-hand goods, review the VAT Margin Scheme.

- If you buy major assets, check the VAT Capital Goods Scheme rules.

The goal is not to choose the easiest VAT scheme. It is to choose the VAT setup that best matches how money actually moves through your business.

This guide is for general information only and is not tax advice. VAT rules can change, and the right scheme depends on your business circumstances. Always check HMRC guidance or speak to a qualified accountant before changing VAT schemes.

What are VAT schemes in the UK?

VAT schemes are HMRC-approved methods that change how VAT-registered businesses calculate, report, or pay VAT. A VAT scheme does not remove VAT obligations, but it can simplify bookkeeping, improve cash flow timing, or reduce administrative pressure when used correctly.

Most VAT-registered businesses in the UK still need to:

- charge VAT on taxable sales

- submit VAT returns to HMRC

- reclaim VAT on eligible business purchases

The standard UK VAT rate is currently 20%, although some goods and services are reduced-rated, zero-rated, exempt, or outside the scope of VAT.

Businesses usually need to register for VAT once taxable turnover exceeds the VAT registration threshold of £90,000 over a rolling 12-month period.

Eligibility thresholds are not the same as exit thresholds. A business may need to leave a VAT scheme if turnover grows beyond the relevant HMRC limit.

For many UK SMEs, the real question is not only:

“Do we need to register for VAT?”

It is also:

“Which VAT scheme will make cash flow and compliance easier to manage?”

That is why choosing the right VAT scheme matters.

Why do VAT schemes matter for UK SMEs?

VAT affects more than compliance. It directly impacts cash flow, bookkeeping workload, pricing decisions, and how much money your business needs to set aside for HMRC.

The wrong VAT setup can make a profitable business feel short of cash.

Many founders only think seriously about VAT when a return deadline is approaching. In reality, VAT problems often begin much earlier through late customer payments, weak bookkeeping, or poor cash flow planning.

VAT schemes become especially important when:

- customers pay invoices late

- VAT is due before cash arrives

- your business has seasonal income

- you sell second-hand goods, antiques, or collectibles

- you buy expensive equipment or property

- you want simpler VAT administration

The right VAT scheme can reduce administrative pressure and improve cash flow visibility, but it should be reviewed regularly as the business grows.

Comparison of VAT schemes for UK small businesses

Scheme | Best suited for | Main benefit | Key consideration |

Smaller VAT-registered businesses with simple costs | Simpler VAT calculation | May not suit businesses with high VATable costs | |

Businesses with late-paying customers | VAT is paid when customers pay invoices | VAT on purchases can only be reclaimed after suppliers are paid | |

Businesses wanting fewer returns | One VAT return per year | Advance instalment payments still apply | |

Sellers of eligible second-hand goods, art, antiques, and collectibles | VAT is charged only on the profit margin | Detailed stock and sales records are required | |

VAT Capital Goods Scheme | Special rule for businesses buying qualifying high-value assets | Adjusts VAT recovery over time

| Usually only relevant where large assets or mixed taxable/exempt use are involved.

|

VAT Flat Rate Scheme explained for small businesses

The VAT Flat Rate Scheme allows eligible VAT-registered businesses to pay VAT as a fixed percentage of VAT-inclusive turnover.

Instead of calculating VAT separately on each sale and purchase, the business applies a fixed flat-rate percentage based on its industry sector.

HMRC designed the scheme to simplify VAT reporting and bookkeeping for smaller businesses.

Businesses can usually join the VAT Flat Rate Scheme if their expected VAT taxable turnover is £150,000 or less, excluding VAT, over the next 12 months.

How does the VAT Flat Rate Scheme work?

Under the VAT Flat Rate Scheme, businesses apply an HMRC-set percentage to total VAT-inclusive turnover.

The percentage depends on the type of business activity.

HMRC also applies a higher 16.5% flat rate to “limited cost businesses” that spend very little on qualifying goods.

For some service-based businesses, such as consultants, designers, or agencies, the scheme may reduce bookkeeping time and simplify VAT returns.

However, simpler administration does not always mean lower VAT costs.

The VAT Flat Rate Scheme may suit businesses that:

- have relatively low VATable expenses

- want simpler VAT administration

- have straightforward bookkeeping

- mainly sell services instead of goods

It may be less suitable for businesses that:

- buy significant stock or equipment

- regularly reclaim large amounts of VAT

- qualify as limited cost businesses

- operate with tight profit margins

Founder takeaway

The VAT Flat Rate Scheme can simplify VAT reporting, but it should always be compared against standard VAT accounting using real business numbers before making a decision.

VAT Cash Accounting Scheme explained

The VAT Cash Accounting Scheme allows eligible businesses to pay VAT to HMRC only after customers pay their invoices, rather than when the invoices are issued.

Businesses using the scheme can also reclaim VAT on purchases only after paying their suppliers.

This approach can help businesses manage cash flow more effectively, especially when customers regularly pay on 30, 60, or 90-day terms.

Under standard VAT accounting, businesses may need to pay VAT to HMRC before receiving payment from customers. For growing SMEs, that timing gap can create unnecessary cash flow pressure.

Businesses can usually join the VAT Cash Accounting Scheme if their VAT taxable turnover is £1.35 million or less.

When is the VAT Cash Accounting Scheme useful?

The VAT Cash Accounting Scheme is often most useful for businesses that invoice customers before receiving payment.

It helps align VAT payments more closely with actual cash entering the business.

The scheme may suit businesses that:

- regularly deal with late-paying customers

- invoice on credit terms

- want VAT payments to reflect real cash flow

- are growing but managing tight working capital

It may be less suitable for businesses that:

- receive customer payments immediately

- pay suppliers slowly

- regularly reclaim large amounts of VAT

- rely heavily on fast VAT recovery from purchases

Founder takeaway

For many UK SMEs, the VAT Cash Accounting Scheme is one of the most practical VAT schemes because it reduces the risk of paying VAT on income that has not yet been received.

VAT Annual Accounting Scheme explained

The VAT Annual Accounting Scheme allows eligible businesses to submit one VAT return per year instead of filing quarterly VAT returns.

Instead of making four separate VAT payments during the year, businesses make advance instalment payments towards their expected VAT bill and then submit a final annual VAT return to reconcile the balance.

According to HMRC guidance, businesses usually make:

- nine monthly instalments, or

- three quarterly instalments towards their estimated annual VAT liability.

The scheme is designed to simplify VAT administration and reduce the pressure of quarterly VAT return deadlines.

However, it does not remove the need for ongoing bookkeeping or VAT planning throughout the year.

Who should consider the VAT Annual Accounting Scheme?

The VAT Annual Accounting Scheme may suit businesses that want:

- fewer VAT return deadlines

- more predictable VAT payment planning

- regular instalment-based budgeting

- a simpler VAT reporting schedule

It may work well for businesses with:

- relatively stable turnover

- predictable VAT liabilities

- consistent bookkeeping systems

It may be less suitable for businesses that:

- experience large monthly income fluctuations

- find VAT liabilities difficult to forecast

- prefer more frequent financial reviews

- regularly reclaim VAT repayments

The VAT Annual Accounting Scheme can reduce administrative pressure for some SMEs, but accurate bookkeeping and cash flow planning still remain important.

VAT Margin Scheme explained

The VAT Margin Scheme allows eligible businesses to pay VAT only on the difference between an item’s purchase price and selling price, rather than on the full selling price.

The scheme may apply to:

- second-hand goods

- works of art

- antiques

- collectors’ items

Under HMRC rules, VAT is usually calculated as one-sixth (16.67%) of the profit margin.

The scheme is particularly important for resale businesses because many second-hand items are purchased from private individuals or non-VAT-registered sellers where VAT was not originally charged.

Without the Margin Scheme, VAT on the full resale value could significantly reduce profit margins.

Who can use the VAT Margin Scheme?

The VAT Margin Scheme is mainly used by businesses that buy and resell eligible second-hand goods, artwork, antiques, or collectibles.

According to HMRC guidance, the scheme cannot usually be used for:

- items bought with VAT already charged

- precious metals

- investment gold

- precious stones

The scheme may suit businesses that:

- sell second-hand goods

- operate antiques or collectibles businesses

- buy stock from private individuals

- generate profit mainly through resale margins

It may be less suitable for businesses that:

- mainly sell new goods

- regularly buy VAT-charged stock

- cannot maintain detailed stock records

- sell goods excluded from the scheme

Record keeping is especially important under the VAT Margin Scheme.

HMRC requires businesses to keep detailed purchase and sales records for items sold under the scheme, and VAT records generally need to be retained for at least six years.

Among UK VAT schemes, the Margin Scheme is one of the most closely linked to the specific type of goods being sold.

VAT Capital Goods Scheme explained

The VAT Capital Goods Scheme applies when a business reclaims VAT on certain high-value assets and the taxable use of those assets changes over time.

Unlike simpler VAT schemes aimed at reducing administration, the Capital Goods Scheme mainly applies to larger purchases, developments, or long-term business assets.

According to HMRC guidance, qualifying capital items can include:

- land and buildings

- civil engineering works

- computer equipment

- aircraft, ships, boats, or vessels

HMRC guidance also includes example value thresholds such as:

- £250,000 or more for land, buildings, and civil engineering works

- £50,000 or more for computer equipment, aircraft, ships, boats, or vessels

When does the Capital Goods Scheme matter?

The Capital Goods Scheme may become relevant when:

- a business reclaims VAT on a qualifying high-value asset

- the business use of that asset changes over time

- the business makes both taxable and exempt supplies

- commercial property or major equipment is purchased or developed

Because the rules are more technical and the amounts involved are often larger, professional VAT advice is usually recommended when the Capital Goods Scheme applies.

Which VAT scheme is best for your business?

The best VAT scheme is the one that matches your cash flow, turnover, cost structure, and type of sales. There is no single best option for every UK SME.

Use this simple decision guide.

Your situation | Scheme to review first | Why |

Customers pay slowly | VAT cash accounting scheme | VAT follows customer payments |

You want simpler small business VAT admin | VAT flat rate scheme | Fixed percentage calculation |

You want fewer VAT returns | VAT annual accounting scheme | One return per year |

You sell eligible second-hand goods | VAT margin scheme | VAT based on margin |

You buy high-value qualifying assets | VAT Capital Goods Scheme | Adjusts VAT recovery over time |

A founder-friendly rule:

If cash flow is the pain, start with cash accounting. If admin is the pain, review flat rate or annual accounting. If your goods are unusual, check margin rules. If the asset is large, get advice.

That is the practical way to compare VAT schemes UK founders are most likely to encounter.

Common mistakes founders make with VAT schemes

The most common VAT mistake is choosing a scheme once and never reviewing it. Your business changes, and your VAT setup should change with it.

1: Choosing simplicity without checking the numbers

The VAT flat rate scheme can feel easier, but a business with meaningful VATable costs may lose out if it cannot reclaim VAT in the usual way.

2: Forgetting cash timing

A profitable invoice is not useful if the cash arrives after the VAT is due. The VAT cash accounting scheme can reduce that timing pressure for eligible businesses.

3: Treating margin scheme records casually

The VAT margin scheme is useful, but only if your records are strong enough to support the calculation.

4: Ignoring asset use changes

The capital goods scheme VAT rules can create adjustments after the original purchase. This is easy to miss when a property or major asset changes use.

5: Thinking VAT is only a tax return issue

VAT affects pricing, cash flow, customer contracts, payment terms, and bookkeeping. The right system starts before the return is due.

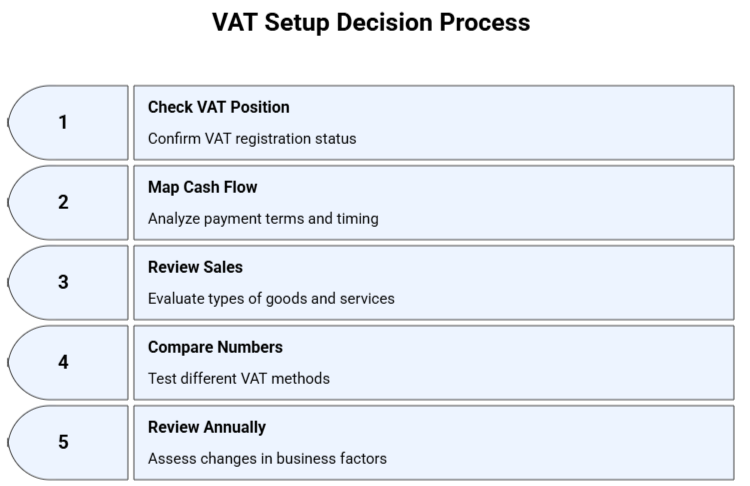

How to choose the right VAT setup in 5 steps

AMS can help UK SMEs review VAT scheme suitability, prepare VAT returns, maintain digital bookkeeping records, and understand the cash flow impact of VAT before deadlines arrive.

Final takeaway

VAT schemes are not shortcuts. They are systems. The right scheme can make VAT clearer, easier, and better aligned with your cash flow. The wrong scheme can create hidden pressure, especially when your business grows.

For UK founders, the aim is not to become a VAT expert. The aim is to understand enough to ask better questions, choose the right setup, and avoid surprises from HMRC.

AMS Admin Services helps UK SMEs turn VAT from a deadline problem into a clear, manageable process.

FAQs

1. What are VAT schemes?

VAT schemes are HMRC-approved methods for calculating, reporting, or paying VAT. They include options such as the Flat Rate Scheme, Cash Accounting Scheme, Annual Accounting Scheme, Margin Scheme. Businesses buying high-value assets may also need to consider the VAT Capital Goods Scheme.

2. Which VAT scheme is best for a small business?

The best VAT scheme for a small business depends on cash flow, turnover, costs, and what the business sells. Service businesses with low costs may review the Flat Rate Scheme, while businesses with late-paying customers may review Cash Accounting.

3. Can I change VAT schemes later?

Yes, many businesses can change VAT schemes if they meet HMRC conditions, but the timing and rules depend on the scheme. It is sensible to review your VAT setup before switching, especially if your turnover, costs, or sales model has changed.